When you apply for business financing, your application goes through a detailed review known as underwriting. Business loan underwriters are responsible for evaluating risk, assessing repayment ability, and determining whether your company qualifies for funding. Their decision directly influences whether you receive approval, what loan amount you qualify for, and what interest rate you are offered.

Understanding what underwriters evaluate—and how they make decisions—gives you a strategic advantage. Many business owners struggle with loan denials simply because they don’t understand the criteria lenders use. This guide explains the underwriting process step by step, highlights the exact factors underwriters analyze, and shows you how to prepare for fast approval.

If you want to see typical financing criteria, review essential business loan requirements.

Key Summary Points

- Underwriting = risk assessment. Lenders analyze repayment ability, stability, and collateral to price risk and set terms.

- Big five signals: creditworthiness, cash flow/DSCR, debt load (DTI), collateral/LTV, time in business & industry risk.

- Documents matter most: P&L, balance sheet, bank statements, tax returns, licenses, ownership docs—organized and consistent.

- Fast wins: improve credit utilization, stabilize monthly cash flow, reduce revolving debt, and reconcile statements.

- Match loan type to profile: banks/SBA = deeper review, online lenders = faster approvals but higher rates.

- Avoid red flags: NSFs, cash deposit spikes, tax liens, big swings in revenue, unverified figures.

- Action links: Check application requirements, required loan documents, and how to improve credit before applying.

What Is Business Loan Underwriting?

Business loan underwriting is a structured risk-assessment process used by lenders to evaluate whether a business is likely to repay borrowed funds. The underwriter’s role is to examine financial documents, credit profiles, revenue patterns, cash flow behavior, debt obligations, and the stability of the business model.

Underwriters focus on two core questions:

- What is the probability that the borrower will repay on time?

- How much financial risk will the lender take by approving the loan?

The underwriting approach varies across lending institutions:

• Traditional banks perform intensive manual underwriting, review multiple years of financial history, and often require collateral.

• SBA lenders follow both lender and SBA guidelines, making the process more documentation-heavy.

• Alternative and online lenders rely on automated underwriting, bank-feed analysis, artificial intelligence, and accelerated decision models, often approving loans within 24–72 hours.

Underwriting ensures fair, risk-based lending while protecting both lenders and borrowers.

What Do Business Loan Underwriters Evaluate During Approval?

Business loan underwriters use a holistic, multi-factor evaluation model. Instead of relying on a single metric, they review a broad range of financial and operational indicators to determine eligibility and risk.

Below is a detailed breakdown of the factors that matter most.

1. Creditworthiness (Personal + Business)

Your creditworthiness is one of the strongest indicators of repayment ability. Underwriters review:

Personal Credit

For small businesses, personal credit reflects your history with debt and financial responsibility. Underwriters examine:

• Payment history• Credit utilization• Length of credit history• Credit mix• Recent inquiries

• Derogatory marks

A strong personal credit score signals reliability and reduces perceived risk.

Business Credit

If your business is established, underwriters will also review:

• Business credit score• Vendor payment history• Credit lines with suppliers• UCC filings

• Trade credit performance

Higher credit scores help qualify for lower interest rates and better terms.

If you need guidance, refer to this internal resource on improving credit score.

2. Cash Flow Strength and Revenue Consistency

Underwriters analyze your revenue behavior, cash flow cycles, and liquidity. Their goal is to determine whether your business generates sufficient free cash flow to cover loan payments.

They review:

• Monthly gross revenue• Net operating income• Cash flow statement trends• Seasonality patterns• Bank-account inflow/outflow activity• Deposits consistency

• Average daily balance

Underwriters also calculate critical financial ratios such as:

Debt Service Coverage Ratio (DSCR)

DSCR = Net Operating Income ÷ Total Debt Obligations

A DSCR above 1.25 is generally considered strong.

Operating Margin & Net Margin

Healthy margins indicate financial efficiency and repayment strength.

Businesses with reliable monthly revenue, positive cash flow, and predictable cycles are considered lower-risk borrowers.

3. Collateral and Business Assets

For secured loans, underwriters evaluate the assets backing the loan. Collateral reduces lender risk and improves the borrower’s loan terms.

Accepted collateral often includes:

• Commercial real estate• Vehicles• Heavy equipment• Inventory• Accounts receivable• Business machinery

• Investment assets

Underwriters assess the asset’s market value, condition, depreciation, and liquidation potential. Appraisals may be required for large loans.

Businesses without collateral still qualify for unsecured financing but often need stronger credit or higher revenue.

4. Debt-to-Income Ratio (DTI) and Existing Obligations

Underwriters evaluate how much of your revenue is currently used for debt repayment. Even strong revenue can be overshadowed by excessive debt.

DTI considers:

• Monthly existing loan payments• Lease obligations• Equipment financing• Credit card balances• MCA daily/weekly deductions

• Lines of credit usage

A DTI under 40–50% is preferred. Lower ratios indicate healthier financial capacity for additional borrowing.

5. Business Age, Stability, and Operating History

The longer your business has been operating, the more confidence an underwriter has in its sustainability. Underwriters analyze:

• Years in business• Revenue growth year-over-year• Industry risk level• Customer demand consistency• Economic exposure

• Operational stability

Banks and SBA lenders prefer businesses at least two years old, but alternative lenders approve startups more easily if other metrics are strong.

6. Industry Risk Level

Some industries have higher default risks, regulatory pressures, or volatility. Underwriters reference risk classifications and internal scoring models to determine:

• Industry failure rates• Revenue volatility• Licensing complexities• Seasonal dependence

• Competition levels

Examples of “higher-risk” industries include:

• Restaurants• Construction• Transportation• Retail

• Hospitality

While high-risk industries aren’t disqualified, they undergo deeper underwriting analysis.

7. Financial Documentation Accuracy and Consistency

Underwriters verify that the information submitted is accurate, consistent, and free from discrepancies. Missing or mismatched data is a common reason for delays or denials.

If you need guidance on documentation, refer to this internal resource on loan documents.

Documents Business Loan Underwriters Review

Underwriters rely on documentation to validate your financial stability and risk level. A complete and well-organized document package significantly increases the likelihood of faster approval.

Below are the primary documents underwriters review.

1. Personal Identification and Credit Background

Underwriters verify identity and assess credit reliability.

They review:

• Government-issued ID• Social Security Number (SSN)• Personal credit reports

• Personal tax returns (2–3 years)

Personal financial history is especially important for startups, sole proprietors, and new LLCs.

2. Business Legal and Registration Documents

These documents confirm that your business is legitimate, compliant, and authorized to operate.

Underwriters review:

• Employer Identification Number (EIN)• Articles of Incorporation/Organization• Business licenses and permits• Ownership agreements• Operating agreements

• Shareholder documents

These ensure legal structure transparency and regulatory compliance.

3. Business Financial Statements

Financial statements offer a clear picture of operational performance and profitability.

Underwriters analyze:

Profit & Loss (P&L) Statement

Reveals revenue behavior, cost structure, and net profitability.

Balance Sheet

Shows assets, liabilities, equity, and financial leverage.

Cash Flow Statement

Demonstrates liquidity, cash generation, and financial resilience.

Strong, stable financials increase approval odds and loan amount eligibility.

4. Business Bank Statements

Bank statements validate real-time financial activity. Underwriters examine:

• Average daily balance• Monthly deposits• Large or irregular deposits• Returned payments• Daily cash flow patterns• Seasonality indicators

• Overdraft frequency

Banks typically require 6–12 months of statements; alternative lenders require 3–6 months.

5. Business & Personal Tax Returns

Tax returns provide verified financial data. Underwriters compare returns with P&L statements to check for consistency.

They review:

• Business tax returns (2–3 years)• Personal tax returns (as needed)

• Schedules & attachments

Tax transparency increases lender confidence.

6. Collateral Documentation (When Applicable)

For assets used as collateral, underwriters review:

• Equipment titles• Property deeds• Inventory reports• Invoice financing documents• Appraisals

• Insurance coverage

Collateral improves the borrower’s loan terms and reduces lender exposure.

How the Business Loan Underwriting Process Works?

While each lender has its own approach, underwriting usually follows a consistent workflow. Below is a step-by-step breakdown.

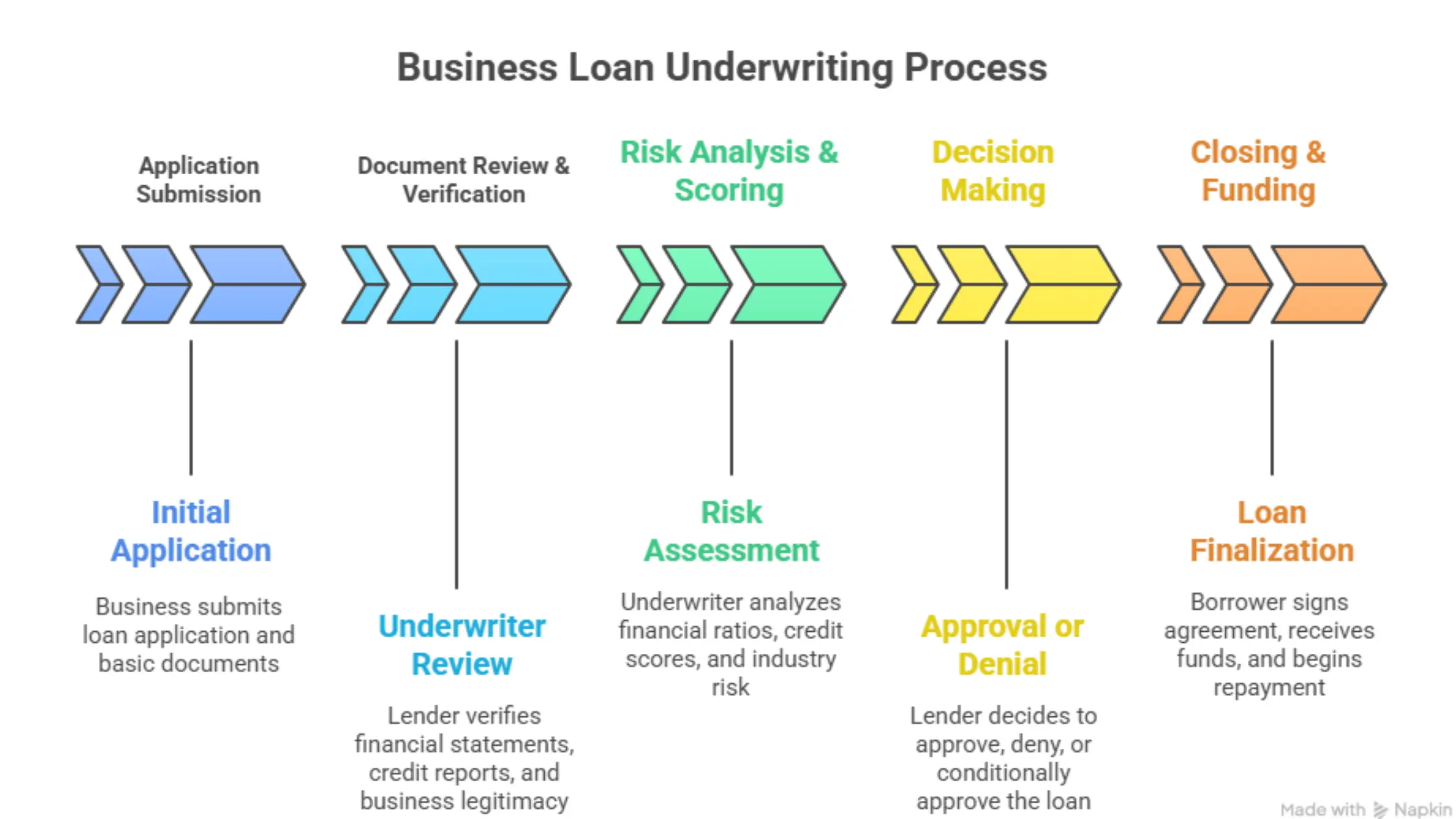

Step 1: Application Submission

The underwriting process begins when you submit your loan application along with basic business information, revenue details, requested loan amount, and preliminary documents.

Underwriters check:

• Eligibility• Business type• Basic financial strength

• Required documentation

If anything is incomplete, they request clarification or additional paperwork.

Step 2: Document Review and Verification

Underwriters review your financial statements, credit reports, bank statements, tax history, and legal documents to validate accuracy.

They verify:

• Revenue consistency• Creditworthiness• Debt levels• Cash flow health• Licensing and registration

• Business legitimacy

Underwriters may also use third-party data sources to confirm business activity, revenue signals, and credit events.

Step 3: Risk Analysis and Scoring

Underwriters assess overall risk using financial ratios, credit scoring models, and industry comparisons. If the lender uses automated underwriting, AI systems analyze data instantly.

Key metrics include:

• DSCR• DTI ratio• Credit utilization• Average bank balance• Revenue volatility• Profit margins• Payment history

• Industry risk tier

Automated underwriting may also analyze:

• Real-time banking data• Cash-flow projections• Seasonality mapping• Merchant deposit frequency

• Risk-based pricing algorithms

Higher risk may trigger additional documentation requests.

Step 4: Decision Making (Approval, Denial, or Conditions)

After reviewing all information, underwriters decide whether to approve the loan.

Possible outcomes:

Approval

You receive a loan offer detailing the amount, term length, interest rate, and repayment structure.

Denial

If denied, the lender provides reasons such as insufficient cash flow, poor credit, high DTI, or inconsistent financials.

Conditional Approval

Underwriters may approve with conditions such as:

• Additional collateral• Co-signer• Lower loan amount• Higher interest rate

• Additional documentation

Step 5: Closing and Funding

Once all conditions are met, the lender finalizes the loan.

You will:

• Sign the loan agreement• Confirm repayment schedule

• Receive the funds (direct deposit)

Repayment begins according to the agreed terms.

Common Reasons Business Loan Applications Get Denied

Underwriting denials often occur due to issues that borrowers can fix with preparation. Common reasons include:

• Low personal or business credit• Insufficient cash flow• High debt obligations• Missing documentation• Inconsistent revenue• Frequent overdrafts• Negative bank balance days• Tax discrepancies• High industry risk

• Unverifiable income

Fixing these issues significantly increases the chance of approval.

How to Prepare Your Business Before Underwriting?

Preparation can dramatically improve underwriting outcomes. Below are key steps:

1. Strengthen Your Cash Flow

• Reduce unnecessary expenses• Increase working capital• Improve revenue consistency

• Build reserve balances

2. Lower Your DTI and Pay Down Debts

Reducing debt obligations enhances your borrowing capacity.

3. Improve Your Credit Profile

• Lower credit utilization• Pay bills on time• Dispute inaccuracies

• Avoid new inquiries

4. Organize Your Financial Documents

Make sure your statements, P&L reports, and tax filings align accurately.

5. Separate Personal and Business Finances

Underwriters prefer dedicated business bank accounts.

6. Prepare Explanations for Irregularities

If you have seasonal revenue dips, overdrafts, or unusual gaps, proactively explain them.

Summary Table: What Underwriters Analyze

CategoryWhat Underwriters CheckWhy It MattersCreditworthinessPersonal + business creditPredicts repayment behaviorCash FlowBank statements, P&L, DSCRDetermines affordabilityDebt LevelsDTI, existing obligationsMeasures financial strainCollateralAssets, appraisalsReduces lender riskFinancial HistoryTax returns, statementsConfirms stabilityIndustry RiskBusiness type, volatilityPredicts long-term survivalOperational HistoryYears in businessShows business maturity

Conclusion

Business loan underwriters evaluate multiple factors including creditworthiness, cash flow, financial stability, debt obligations, and industry risk. By understanding how underwriting works—and preparing your financials strategically—you significantly increase your chances of approval, qualify for better loan terms, and shorten the funding timeline.

Purple Tree Funding makes the underwriting process simpler, faster, and more accessible. Our flexible programs, streamlined document requirements, and personalized support help business owners secure the capital they need with confidence.

Start your application today and position your business for growth with the right financing.

FAQs About Business Loan Underwriting

Q1. How long does underwriting take?

Depending on lender type, underwriting can take anywhere from 24 hours (alternative lenders) to several weeks (banks/SBA).

Q2. Do underwriters check both personal and business credit?

Yes. Personal credit is crucial for new businesses; business credit becomes more important for established companies.

Q3. Can you get approved with bad credit?

Yes. Some lenders allow low-credit borrowers if cash flow is strong or collateral is available.

Q4. What documents do underwriters review?

They verify bank statements, tax returns, financial statements, business licenses, and collateral documentation.

Q5. Can you speed up the underwriting process?

Submitting complete, accurate documents and responding quickly to lender requests speeds up approval.

Q6. What if my application is denied?

You can fix the issues (e.g., improve credit, increase cash flow, lower debt) and reapply later.