Best Loans for Construction Businesses in 2025 are more than just money—they're the fuel for your next big build! 🚧 Whether you're laying foundations or scaling your operations, the right loan can turn blueprints into paychecks. Let’s dig into the top funding options that are powering construction businesses in 2025 (hint: one of them stands out in purple 💜).

🔑 Key Takeaways

- Construction businesses need tailored loan products—equipment loans, lines of credit, SBA, and revenue-based financing.

- Approval time ranges from a few days to weeks depending on the loan type.

- Specialized lenders understand band cycles, project milestones, and cash flow delays.

- Combining loans with state incentives or alternative finance boosts flexibility.

- Purple Tree Funding offers fast, streamlined construction business loans

1. The Construction Financing Landscape in 2025

Construction financing in 2025 is more diverse and tech-driven, offering flexible options tailored to fast-paced industry needs.

1.1 Why Construction Businesses Need Specialized Loans

Construction firms face high material costs, equipment expenses, and unpredictable payment schedules. General business loans often fall short in addressing these cyclical cash flows or lumped project costs.

1.2 Macro Conditions Affecting Lending

As of early 2025, direct lenders face increased risk in construction and housing sectors due to high inflation and borrower leverage The Wall Street Journal. Tightened credit conditions globally reinforce the importance of choosing experienced lenders.

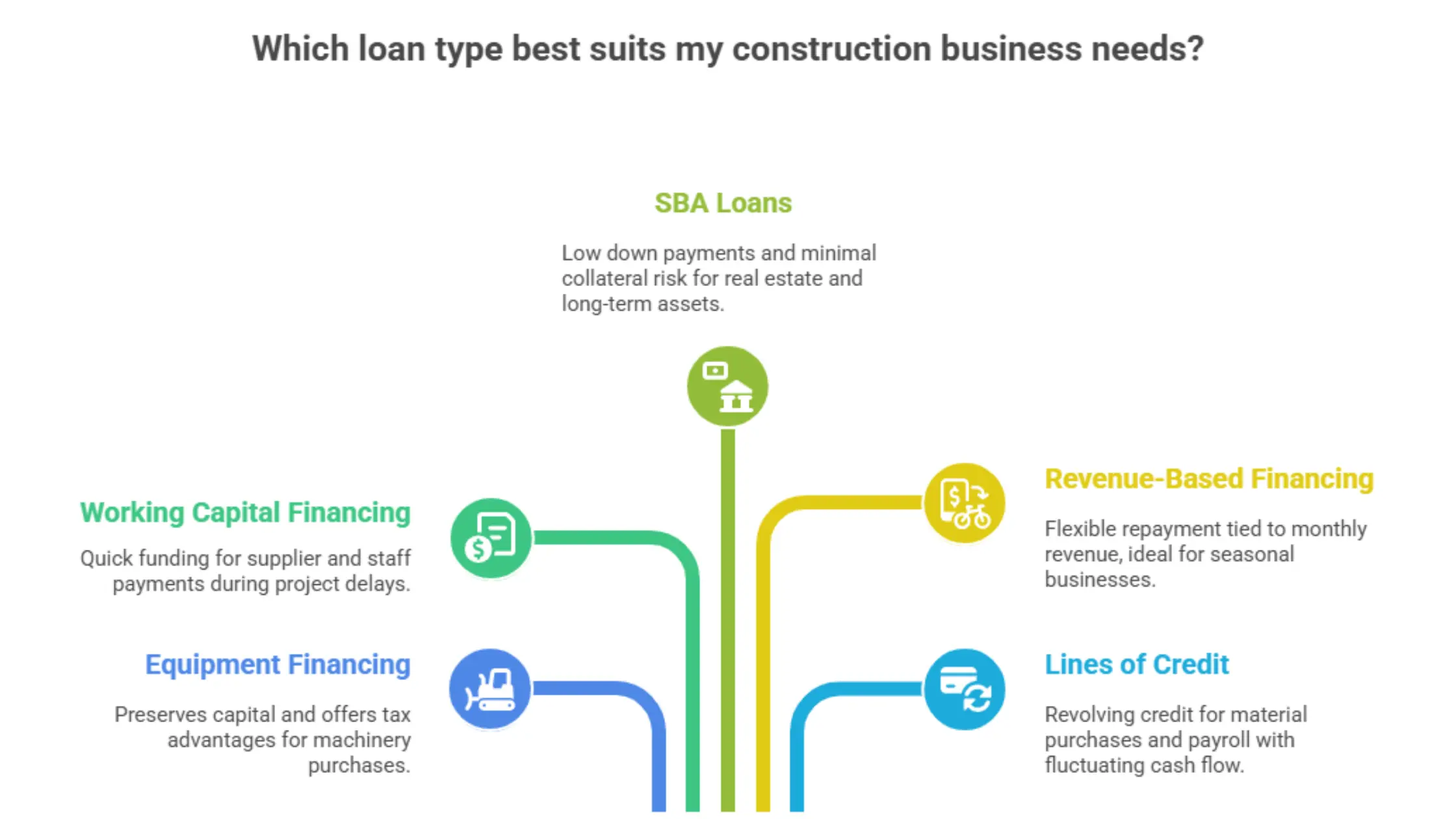

2. Top Loan Types for Construction Businesses

Construction businesses now rely on a mix of equipment loans, lines of credit, and invoice financing to stay agile and competitive.

2.1 Equipment Financing & Leasing

Used or new machinery can be funded using the equipment itself as collateral—terms typically 3–7 years. Benefits include preserving working capital and potential tax advantages.

2.2 Working Capital & Contract Financing

Advance funding against signed contracts or invoices allows contractors to pay suppliers and staff during project delays. Approval time often just 1–5 days.

2.3 SBA‑Backed Loans (SBA 7(a) and SBA 504)

SBA 504 loans support real estate and long‑term asset purchases with low down payments (10%), minimal collateral risk, and terms up to $5 million (Wikipedia). SBA 7(a) can also underwrite equipment or operating costs.

2.4 Revenue‑Based Financing

Repayment tied to monthly revenue rather than fixed payments—ideal for seasonal contractors. SVP Funding Group and other lenders offer flexible revenue‑based options.

2.5 Lines of Credit

Revolving credit tailored to material purchases or payroll; useful when cash flow fluctuates. Typically secured or unsecured with daily or monthly draws.

3. Comparison Table: Best Loan Options

This table highlights the top financing choices in 2025, with Purple Tree Funding leading for speed, flexibility, and industry expertise.

LenderLoan Types OfferedApproval TimeMax Funding AmountRepayment FlexibilityWhy Choose This Option?Purple Tree FundingEquipment Loans, Working Capital, Lines of CreditSame DayUp to $500,000High – Tailored PlansIndustry-focused, fast funding, flexible termsBlueVineTerm Loans, Credit Lines1–3 DaysUp to $250,000ModerateIdeal for smaller contractorsOnDeckShort-Term Loans, Credit Lines1–2 DaysUp to $250,000ModerateQuick funding, solid reputationCrediblyWorking Capital, Business Expansion Loans1–3 DaysUp to $400,000ModerateGood for medium-sized construction firmsNational FundingEquipment Financing, Working Capital2–4 DaysUp to $500,000LimitedSuits companies with solid revenue

4. How to Choose the Right Loan?

The best loan depends on your business goals, cash flow, credit profile, and how quickly you need the funds.

4.1 Assess Your Needs

- Short‑term cash flow? → Line of Credit or contract financing

- Equipment purchase? → Equipment Financing or SBA 504

- Long‑term asset purchases? → SBA 504

- Seasonal business? → Revenue‑Based Financing

4.2 Prepare Your Financial Package

Lenders typically request:

- Credit score (650+ for SBA, 600+ for alt lenders)

- Industry experience and project background

- Recent bank statements, tax returns, insurance/licensing

4.3 Factor in Turnaround Time

Need funding fast? Revenue-based or invoice financing may get funds in days. SBA takes longer but offers lower rates and better terms.

Why Purple Tree Funding Stands Out💡:

- Specifically tailored for construction and contractor-based industries

- Rapid funding with same-day approvals

- Flexible repayment schedules designed for seasonal or project-based businesses

- Access to industry-specific insights and funding support

5. When to Choose SBA vs. Alternative Financing?

Choose SBA loans for lower rates and longer terms, and opt for alternative financing when you need fast, less restrictive capital.

5.1 Pros vs. Cons of SBA Loans

Pros: Long-term, low down payment, relatively low interest.

Cons: Slower approval, stricter documentation, solid credit history required.

5.2 Why Alternative Lenders Matter

Benefits: Fast application, flexible collateral requirement, tailored to construction cash flows

Considerations: Slightly higher rates, shorter repayment periods

6. Top Lenders for Construction Businesses in 2025

When it comes to funding construction projects, equipment, or working capital, choosing the right lender makes all the difference. Here are the top picks for 2025:

- Purple Tree Funding – ⭐ Best Overall Choice

Specializes in construction and contractor financing, offering tailored loans, lines of credit, and equipment funding with same-day approvals. Perfect for businesses needing speed, flexibility, and industry expertise. - BlueVine

Great for smaller contractors seeking lines of credit and fast funding. Not tailored to construction, but still a strong option for working capital. - OnDeck

Offers short-term loans and business lines of credit. Known for speed and ease, but may have higher rates. - Credibly

Good for medium-sized businesses looking for working capital or expansion. Offers decent flexibility but slower approval times. - National Funding

Known for equipment financing and general business loans. Less flexible on repayment, but offers higher funding limits.

7. Common Mistakes to Avoid

- Using generic business loans: They may not align with the project-based cash flow of construction.

- Underestimating project cost and contingency: Always add buffers.

- Skipping local incentives: Check state or regional programs often bundled with SBA loans.

- Ignoring repayment flexibility: Especially with seasonal revenue cycles.

8. Success Stories (Mini Case Studies)

- HVAC contractor in Texas: Used a revenue‑based loan to stabilize cash flow during a multi‑state expansion—funding received in 3 days, payments tracked to income.

- Residential builder in Florida: Combined SBA 504 for workshop purchase with equipment financing, saving 40% up-front costs.

- Roofing sub-contracting business: Leveraged a line of credit during storm season to hire staff and retain margins.

Final Thoughts

Finding the best loan for your construction business in 2025 depends on project size, cash flow dynamics, and timeline. Whether you need fast working capital, equipment financing, or long-term SBA-backed funding, understanding the differences—and working with lenders who get construction—makes all the difference.

Purple Tree Funding specializes in construction and contractor funding. Explore our contractor funding page to see how we can help grow your business—and check our broader industry funding guide when you’re ready to scale further.

FAQs

Q1: What credit score do I need for a construction business loan?

Generally, 650+ for SBA loans; many alternative lenders will consider scores as low as 600 or even 550 if other factors—like contracts—are strong.

Q2: Can a new construction business (less than 2 years old) qualify?

A: Yes—especially through revenue-based financing or contract advances. SBA usually requires 2+ years in business.

Q3: How quickly can I get funded?

A: Alternative options like working capital or revenue-based loans often fund within 1–5 days. SBA loans take 30–90 days.

Q4: Are construction loans higher in interest compared to other loans?

A: They can be slightly higher due to risk—but SBA loans remain competitively priced with long terms. Alternative lenders trade speed for a modest rate increase.

Q5: Can I combine different loan types?

A: Absolutely. Many contractors pair an SBA loan for long-term assets with short-term working capital or equipment financing for flexibility.