You’ve put in the hours and built your reputation. Secured the contracts. And now, your electrical business is ready to grow, but the tools holding it all together are outdated. You know you need new equipment, but how you pay for it could make or break your momentum. That’s where business loans for electricians come in. Whether you're a solo operator or running a team of electrical contractors, equipment financing can fuel your next big leap. But only if you avoid the electrician business loan mistakes that catch even experienced business owners off guard.In this guide, we’ll break down the real-world mistakes that electricians make when applying for equipment loans—and how you can sidestep them with confidence and clarity.

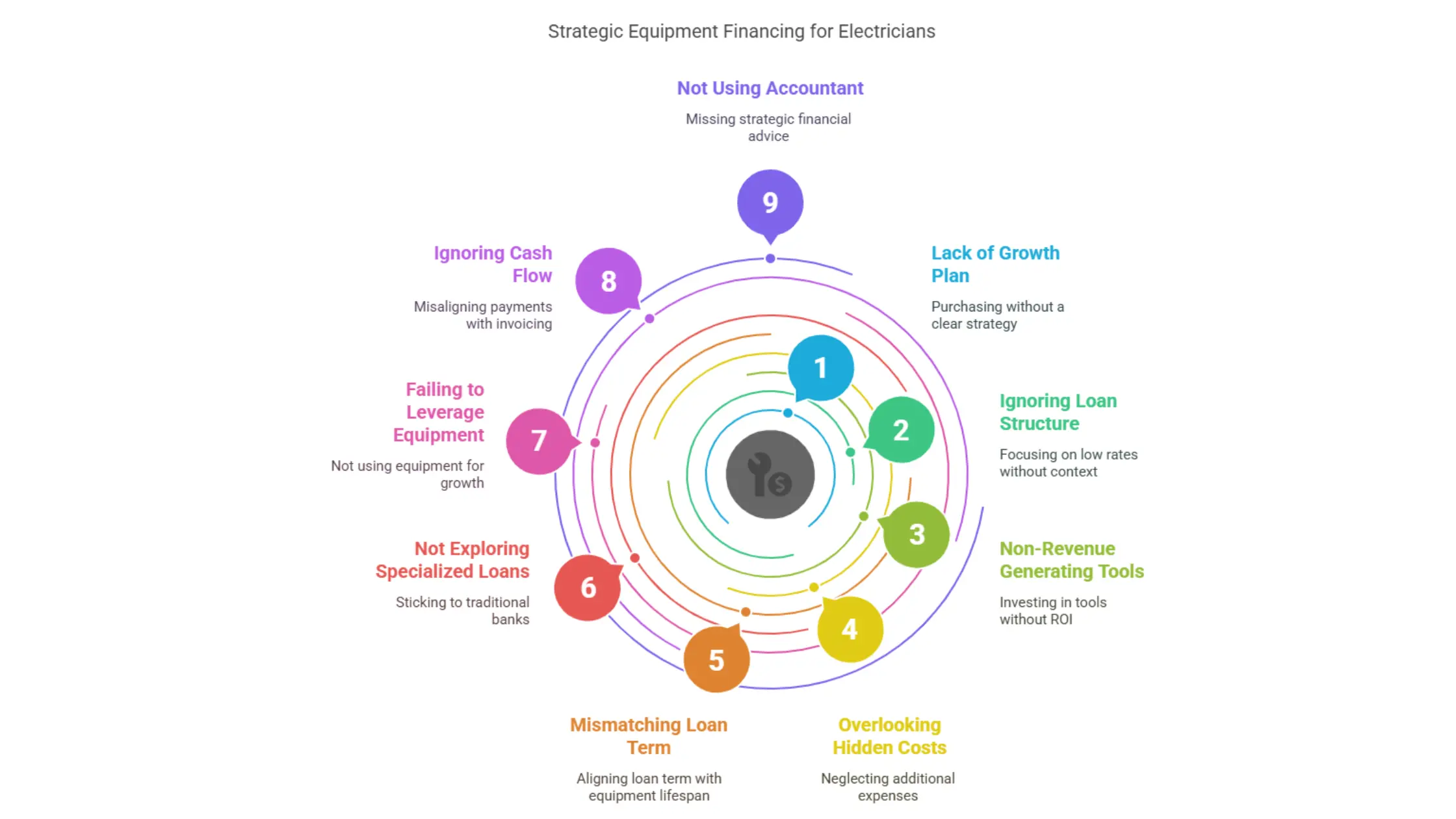

Mistake #1: Buying Equipment Without a Growth Plan

If you want to know how to use an Electrician Business Loan to Grow Your Company, it's basically with a growth plan. It's easy to get excited by a new service van or that top-of-the-line diagnostic tool. But purchasing without a clear growth strategy is like rewiring a panel without a diagram.Too often, electricians borrow for equipment they “might” use rather than what their business model demands today.

Smarter approach:

- Ask: What contracts am I bidding on that require this equipment?

- Project: Will this investment pay off in 12–24 months?

- Prioritize: What’s mission-critical versus what’s nice-to-have?

When you align your financing with your growth plan, every dollar becomes a business accelerator, not just a purchase.

Bonus Read: If you're still refining how to align funding with business expansion, this guide on how to use an electrician business loan offers practical tips for investing with purpose.

Mistake #2: Chasing Low Interest Rates Without Context

We get it, nobody wants to overpay. But obsessing over low interest rates while ignoring the loan structure is a recipe for regret. Some lenders promote ultra-low rates, then bury you in fees, restrictive terms, or balloon payments.Instead, ask:

- Is this equipment loan fixed or variable?

- What are the total repayment costs over time?

- Can I pay off my loan early without incurring penalties?

When comparing electrical business financing options, consider long-term flexibility over flashy numbers. Comparing rates is just the beginning. To make a well-informed choice, it’s worth reviewing the different financing options for electrician businesses and what each one brings to the table.

Mistake #3: Financing Tools That Don’t Generate Revenue

One of the easiest ways to burn through borrowed money is by financing tools that won’t produce an immediate return on investment (ROI). You don’t need every gadget on the shelf. If it’s not helping you land more jobs or finish them faster, think twice before financing it. Stick to equipment that increases output, lets you scale into new job types (like EV charging stations), or makes your team more efficient.

Mistake #4: Overlooking Hidden Costs

Most electrical contractors think only of the equipment price tag. But what about the actual cost of ownership?If you only plan for the monthly loan payment, you might overlook:

- Maintenance and calibration fees

- Training costs for new systems

- Insurance, storage, and upgrades

These extras can pile up quickly. Your electrical contractor business loan should consider the entire picture, not just the invoice price.

Mistake #5: Mismatching Loan Term with Equipment Lifespan

Here’s a classic mistake: financing a laptop or handheld meter over 5 years. If the gear breaks down in two, you're still stuck paying.

Golden rule:

Match your loan term to the realistic life of the asset.Equipment TypeIdeal Loan TermHandheld tools12–24 monthsService trucks3–5 yearsIndustrial generators5–7 yearsDiagnostic equipment2–4 years

Mistake #6: Not Exploring Specialized Electrician Loans

Many electricians default to their bank for financing, but that’s not always the best route.Banks are conservative. If you’ve been in business for under 2 years or have a seasonal cash flow model, you may not get approved.Instead, explore electrician loans from alternative lenders who specialize in trade businesses. They understand your cycle. They tailor repayment. They move fast. Some lenders even offer electrical business funding with same-day approvals and no hard collateral required.Wondering what kind of loan your business qualifies for? This article breaks down how much you can borrow for an electrician business based on factors like credit, revenue, and time in business.

Mistake #7: Failing to Use Equipment as Leverage for More Work

Here's the part most electricians miss: equipment loans aren’t just about tools, and they're about growth. Have a new service van? Use it to expand your service area. Bought upgraded testing gear? Target commercial contracts. Added automation? Reduce labor and quote more jobs.

Pro tip:

Mention your new capabilities in your bids. It sets you apart and shows you’re investing in quality delivery.

Mistake #8: Ignoring Your Cash Flow Realities

Financing that appears favorable on paper may not align with your invoicing cycle. If your jobs are net-30 or net-60 and your payments are weekly, you could fall behind. That’s when a good loan becomes a burden.Look for lenders that:

- Offer seasonal or flexible repayments

- Match payment schedules to your client pipeline

- Understand the realities of contractor cash flow.

Mistake #9: Not Using Your Accountant

Your accountant isn’t just for taxes. They can help structure your equipment loan in ways that maximize deductions (hello, Section 179), minimize debt, and keep your ratios healthy. A great accountant can turn a basic loan into a strategic advantage. If your accountant isn’t involved in your funding conversations, you’re leaving money on the table.For a smoother approval process, it’s essential to know what lenders look for in electrician business loan applications—from financials to business plans.

How to Make Your Business Equipment Loan Work for You?

The goal of electrical business financing isn’t just to buy, but to build. Build capacity, reach and professionalism.Here’s a checklist to help you stay ahead:

- Know precisely what you’re buying and why

- Compare lenders (not just rates)

- Check term-to-lifespan match

- Budget for ownership costs

- Align repayments with revenue.

- Lean on your accountant.

- Use the equipment to unlock more contracts.

Final Thoughts

Business loans for electricians should do more than just buy tools; they should also build momentum. The difference between thriving and treading water often comes down to how, when, and how you choose to invest in your business.So here’s the truth:Every day you delay the right upgrade, you could be losing contracts, falling behind competitors, or burning time on outdated gear. Meanwhile, others are financing smarter and growing faster.But here’s the good news:You don’t have to navigate it alone. Whether you're upgrading a single tool or reequipping your entire crew, the right funding partner makes all the difference. Get a custom plan, not a cookie-cutter offer, with Purple Tree Funding.

FAQs

Q1. What are the best business loan options for electricians?

Electricians can explore options like equipment financing, working capital loans, lines of credit, and specialized trade business loans from alternative lenders. Choosing the right loan depends on business size, equipment needs, and cash flow structure.

Q2. How can I use an electrician business loan to grow my company?

You can use an electrician loan to invest in tools, service vehicles, and advanced diagnostic equipment that help you win bigger contracts, expand your service area, or improve operational efficiency—leading to increased revenue.

Q3. What should I avoid when financing electrician equipment?

Avoid common mistakes like borrowing without a growth plan, chasing only low interest rates, mismatching loan terms with equipment lifespan, and ignoring cash flow timing or hidden costs.

Q4. Are there electrician business loans available for new contractors?

Yes, many alternative lenders offer electrician loans to newer contractors—even those in business for less than two years. These lenders understand trade business models and often provide flexible terms and faster approvals than traditional banks.

Q5. How do I match my loan term to the equipment lifespan?

A good rule is to finance equipment only for the duration it will be useful. For example, handheld tools may need a 1–2 year loan, while a service truck may justify a 3–5 year term. This ensures you're not paying for assets after they become obsolete.