When it comes to securing financing, your credit score can significantly impact your chances. Lenders use it to measure risk, determine approval, and set loan terms. That’s why understanding how to improve your credit score before applying is one of the smartest steps any business owner can take.A higher credit score not only boosts your likelihood of approval but can also unlock better interest rates and larger funding options. On the other hand, a weak score can result in rejections, smaller loan amounts, or higher borrowing costs. The good news? With the right strategy, you can start improving your score in as little as a few months.In this comprehensive guide, Purple Tree Funding explains how to boost your credit score before submitting your application — and what financial strategies can help you get approved with confidence.

Key Takeaway:

To improve your credit score before applying for a loan, review and dispute credit report errors, pay bills on time, lower credit utilization below 30%, and avoid new debt. These actions can boost your score within 30–90 days.

Why Your Credit Score Matters Before Applying for Financing?

When you apply for financing, lenders are taking a calculated risk. Your credit score serves as a shortcut for lenders to evaluate how reliable you are as a borrower. It reflects your past behaviors, such as how often you pay bills on time, the amount of debt you carry, and how responsibly you’ve managed credit lines. For business owners, this number can be the deciding factor between a quick approval with low interest rates or a denial that halts growth plans.

How Lenders View Your Creditworthiness?

When applying for a loan, your credit score helps lenders quickly evaluate risk. Here’s how various lender types weigh it:

Traditional Banks

Banks are the most conservative lenders in the marketplace. For them, credit scores carry significant weight. In most cases, they look for personal credit scores of 680 or higher before approving small business loans. Additionally, they may also request business credit scores, debt-to-income ratios, and collateral to mitigate their risk further. Falling below the preferred score range doesn’t necessarily mean automatic rejection, but it often results in smaller loan offers or higher interest rates.

SBA Loans

The Small Business Administration (SBA) doesn’t lend money directly, but it guarantees loans through partner banks and credit unions. Because of this backing, SBA loans are considered lower risk for lenders, which allows them to offer favorable terms. However, most lenders still expect applicants to have a credit score of at least 640–650. A higher score improves the chances of approval and increases the likelihood of securing larger loan amounts with more flexible repayment terms.For a full list of what’s needed for SBA or other business financing, review our guide on business loan application requirements.

Alternative Lenders

Fintech companies and online lenders have revolutionized the borrowing landscape for borrowers with less-than-perfect credit. Unlike banks, they place more emphasis on real-time cash flow, revenue trends, and business performance. This means even if your credit score is below 650, you may still qualify for financing if your business demonstrates steady income and growth potential. The trade-off is that alternative loans may come with shorter repayment periods or slightly higher rates, but they provide faster access to capital.

Understanding Credit Score Ranges

Knowing where your score falls helps you gauge your eligibility:

Credit Score RangeCategoryLoan Impact750+ExcellentBest rates, highest approval odds700–749GoodFavorable terms, likely approval650–699FairApproval possible with higher ratesBelow 650PoorLimited options, may need alternative funding

- 750+ (Excellent): You’re in the top tier, which usually means instant approvals, the lowest interest rates, and access to the highest loan amounts.

- 700–749 (Good): Strong approval odds with favorable terms, though you may not get the absolute best rates.

- 650–699 (Fair): Approval is possible, but you may face higher rates or stricter loan conditions.

- Below 650 (Poor): Options are limited. Most banks will decline, but alternative lenders may still consider you.

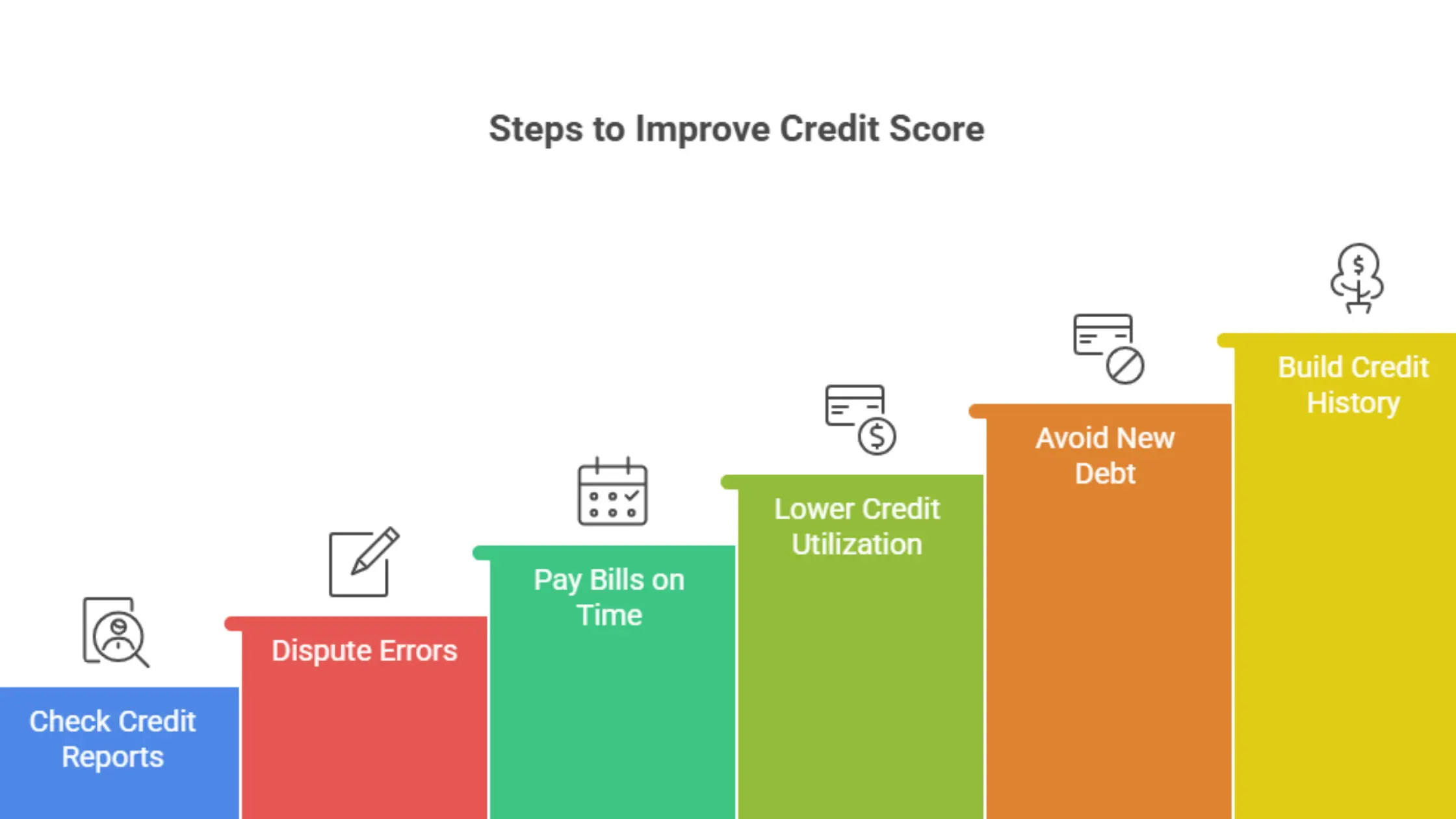

6 Steps to Improve Your Credit Score Before Applying

Improving your credit score doesn’t happen overnight, but with consistent action, you can strengthen your profile before submitting a loan application. Here’s a clear roadmap to follow:

1. Check Your Credit Reports

Start by requesting free copies of your credit reports from Experian, Equifax, and TransUnion. Reviewing them helps you understand where you stand and what lenders will see when they evaluate your application.

If you’re unsure what documents lenders might need when reviewing your credit, check out What Documents Do I Need for a Business Loan.

2. Dispute Errors and Inaccuracies

Mistakes happen. Accounts are reported as late when they were paid on time, or debts are shown as open when they’ve been settled. File disputes with the credit bureaus to correct these errors, as even a single mistake can lower your score significantly.

3. Pay Bills on Time

Your payment history accounts for approximately 35% of your FICO score. Setting up autopay or reminders ensures you never miss a due date. A consistent streak of on-time payments is one of the fastest ways to strengthen your score.

4. Lower Credit Utilization

Lenders want to see that you’re not maxing out your available credit. Aim to keep utilization below 30% of your credit limit across all cards and lines. Paying down balances or requesting higher limits (without new spending) can help lower this ratio.

5. Avoid New Unnecessary Debt

Every time you apply for new credit, it creates a hard inquiry on your report. Receiving too many inquiries within a short period can negatively impact your credit score. Focus on managing existing accounts instead of opening new ones.

6. Build Credit History with Small Accounts

If your credit file is thin, consider:

- Opening a secured credit card.

- Becoming an authorized user on a trusted person’s account.

- Using a small business line of credit responsibly.

These actions gradually build credit depth and repayment reliability.

Business Credit Score Improvement Strategies

While personal credit is essential, many lenders, especially banks and SBA partners, also check your business credit score. A strong business profile shows that your company is financially reliable and capable of managing debt responsibly. Here are steps you can take to strengthen it before applying:

1. Separate Business and Personal Finances

Open a dedicated business checking account and use it exclusively for company transactions. This separation enables lenders to clearly evaluate a business's cash flow without mixing in personal expenses.

2. Apply for a Business Credit Card

Using a business credit card responsibly helps build a credit history tied to your company’s Employer Identification Number (EIN). Keep balances low and pay in full each month to demonstrate sound management.

3. Work with Vendors Who Report to Credit Bureaus

Not all suppliers report payment history. Partner with those who do, and make sure you pay invoices early or on time. This builds your business credit file with agencies like Dun & Bradstreet.

4. Get a D-U-N-S Number

Registering for a D-U-N-S number with Dun & Bradstreet allows you to establish and track your business credit file. Many lenders use this database when reviewing loan applications.

5. Maintain Positive Payment History

Just like personal credit, consistent on-time payments matter most. Whether it’s utility bills, vendor accounts, or lease payments, staying current boosts your business credit score over time.

Common Mistakes to Avoid When Fixing Credit

Improving your credit score takes time, and even minor missteps can slow your progress. To stay on track, here are some of the most common errors borrowers make when trying to repair credit and how to avoid them:

Closing Old Accounts

It may seem wise to close old credit lines, but doing so shortens your credit history and reduces your available credit limit.Fix: Keep older accounts open, even if you don’t use them often. They add length to your credit history and improve utilization ratios.

Applying for Too Much Credit at Once

Each new credit application creates a “hard inquiry” on your report. Multiple inquiries in a short time can signal risk and reduce your score.Fix: Space out applications and only apply for new credit when necessary.

Ignoring Credit Monitoring

Without monitoring, you won’t spot errors, fraudulent activity, or sudden score drops until it’s too late.Solution: Utilize free credit monitoring tools or services offered by bureaus such as Experian, Equifax, or TransUnion to stay informed.

Maxing Out Credit Lines

High balances relative to your credit limits can damage your scores, even if you make timely payments.Fix: Aim to keep credit utilization below 30%. Lower is always better.

Paying Only Minimum Balances

Carrying large amounts of revolving debt signals financial strain and keeps your score from improving.Solution: Pay more than the minimum and target high-interest accounts first to reduce balances more quickly.

How Long Does It Take to Improve a Credit Score?

One of the most common questions borrowers ask is: How fast can I raise my credit score? The truth is, credit improvement is a gradual process that depends on your starting point and the strategies you use. While there are some quick wins, building lasting credit strength takes time.

Short-Term Improvements (30–90 Days)

- Disputing errors on your credit report

- Paying down revolving balances

- Reducing credit utilization

- Making all payments on time for a few months

These steps can give your score a noticeable boost in as little as a few weeks, especially if your utilization has been high or errors exist on your report.

Medium-Term Improvements (6–12 Months)

- Establishing consistent on-time payments

- Keeping utilization below 30% for several months

- Building a record with a secured credit card or small business credit account

During this time, lenders start to see a pattern of reliability, which strengthens your chances of approval.

Long-Term Improvements (1+ Years)

- Maintaining accounts in good standing

- Keeping old accounts open to lengthen credit history

- Expanding business credit through vendors and trade lines

- Avoiding new unnecessary debt

Over time, these habits can move you from “fair” to “good” or even “excellent,” unlocking access to the best financing options and interest rates.

Preparing for Financing in 2026

Improving your credit score is part of a broader loan readiness strategy. Once you’ve strengthened your profile, it’s time to prepare the necessary paperwork and review your eligibility.

Whether you’re looking to improve credit fast or build long-term financial stability, understanding how credit utilization, payment history, and account age affect your FICO score gives you a clear path to success. Business owners who follow these steps consistently can rebuild credit history and qualify for better financing options.Your credit score plays a crucial role in determining whether lenders approve your request and what interest rate you are offered. By checking your reports, reducing errors, paying bills on time, and enhancing credit utilization, you can strengthen your financial profile before applying. Consistent improvements, whether in personal or business credit, make you a more attractive borrower and open doors to better loan options.If you’re preparing for financing in 2025, now is the time to take action on your credit. When you’re ready to apply, Purple Tree Funding makes the process easier with flexible solutions designed for small businesses. We help you move past roadblocks and access the capital you need to grow with less stress and fewer delays. Apply today and get fast funding!

FAQs About Improving Your Credit Score

Q1. How can I raise my credit score quickly before applying for a loan?

Paying down credit card balances, lowering utilization below 30%, and disputing errors on your credit report are some of the fastest ways to see improvement. Even a 20–30 point increase can help you qualify for better terms.

Q2. Do lenders check both personal and business credit scores?

Yes. For small business loans, lenders often review personal vs business credit together. If your business credit file is thin, your personal credit score may carry more weight.

Q3. Can I still get approved for a loan with a bad credit score?

It’s possible. Traditional banks may decline, but SBA lenders and alternative financing companies sometimes approve borrowers with lower scores if cash flow, revenue, or collateral is strong.

Q4. How long does it usually take to rebuild credit?

Minor improvements can be seen within 1–3 months, but establishing a strong credit history typically takes 6–12 months of consistent on-time payments and responsible account management.

Q5. Should I pay off old debts or focus on current balances first?

Start with high-interest revolving debt, as it has the most significant impact on your credit utilization. Paying off smaller accounts can also help utilization and show positive repayment activity.