Whether you're adding a new imaging suite, covering payroll through a slow insurance-reimbursement cycle, or expanding into a second location, the financing you choose shapes how smoothly your practice runs. Not every medical and healthcare loan is built on the same terms; speed and flexibility vary widely, and the wrong fit can cost you more than the procedure or purchase you're funding. Here are the six things to look for before you sign.

What to Look for in a Medical Practice Financing Partner

Choosing the right lender is just as important as choosing the right financing product. Medical practices need funding that moves quickly, fits healthcare cash flow, and supports specific goals like equipment purchases, working capital, hiring, or expansion. Before applying, compare lenders based on speed, product fit, repayment terms, approval criteria, cost transparency, and healthcare industry experience.

1. Funding Speed That Matches Your Timeline

Medical practices rarely have the luxury of waiting weeks for a decision. Equipment fails, a hiring window opens, or a buildout schedule won't pause for a slow bank. Look for a lender that underwrites on your practice's revenue and cash flow rather than collateral alone; those decisions often land in 24 to 48 hours, with funding shortly after.

Traditional banks move slowly and lean heavily on documentation. If your need is time-sensitive, prioritize a funder built for speed. The fastest approval is worthless if it arrives after the opportunity closes.

2. The Right Product for the Right Need

"Medical loan" is a category, not a single product. Match the structure to what you're actually funding:

- Medical practice financing: Flexible capital for operations, expansion, or general growth

- Medical equipment financing: Tied to a specific purchase like imaging, dental, or diagnostic equipment, often with the equipment securing the loan

- Healthcare working capital: Unrestricted funds for payroll, supplies, or bridging reimbursement gaps

Buying one defined asset points you toward equipment financing. Needing cash to run or grow the practice points toward working capital or broader practice financing. Picking the wrong structure for a fixed-term loan for a recurring cash gap, for example, locks you into payments that don't match how the money's used.

3. Terms That Fit Healthcare Cash Flow

Medical revenue doesn't arrive like retail revenue. Insurance reimbursements lag, patient volume swings seasonally, and large receivables can sit for weeks. Your financing should account for that.

Look for repayment terms that align with your actual cash flow, not a rigid schedule that strains your slow months. Some lenders offer healthcare working capital with flexible repayment that flexes alongside your deposits, which fits the reimbursement rhythm far better than a fixed bank installment.

4. Approval Criteria Built for Medical Practices

Banks often penalize practices for thin hard collateral or a young operating history. Industry-focused lenders weigh different signals, consistent revenue, healthy deposits, and the stability of a healthcare business that isn't going anywhere.

Before applying, ask what actually drives the decision. If the answer centers on your practice's revenue and cash flow rather than a pristine personal credit profile or heavy collateral, you're looking at a lender that understands medical financing. That distinction often decides whether you're approved at all.

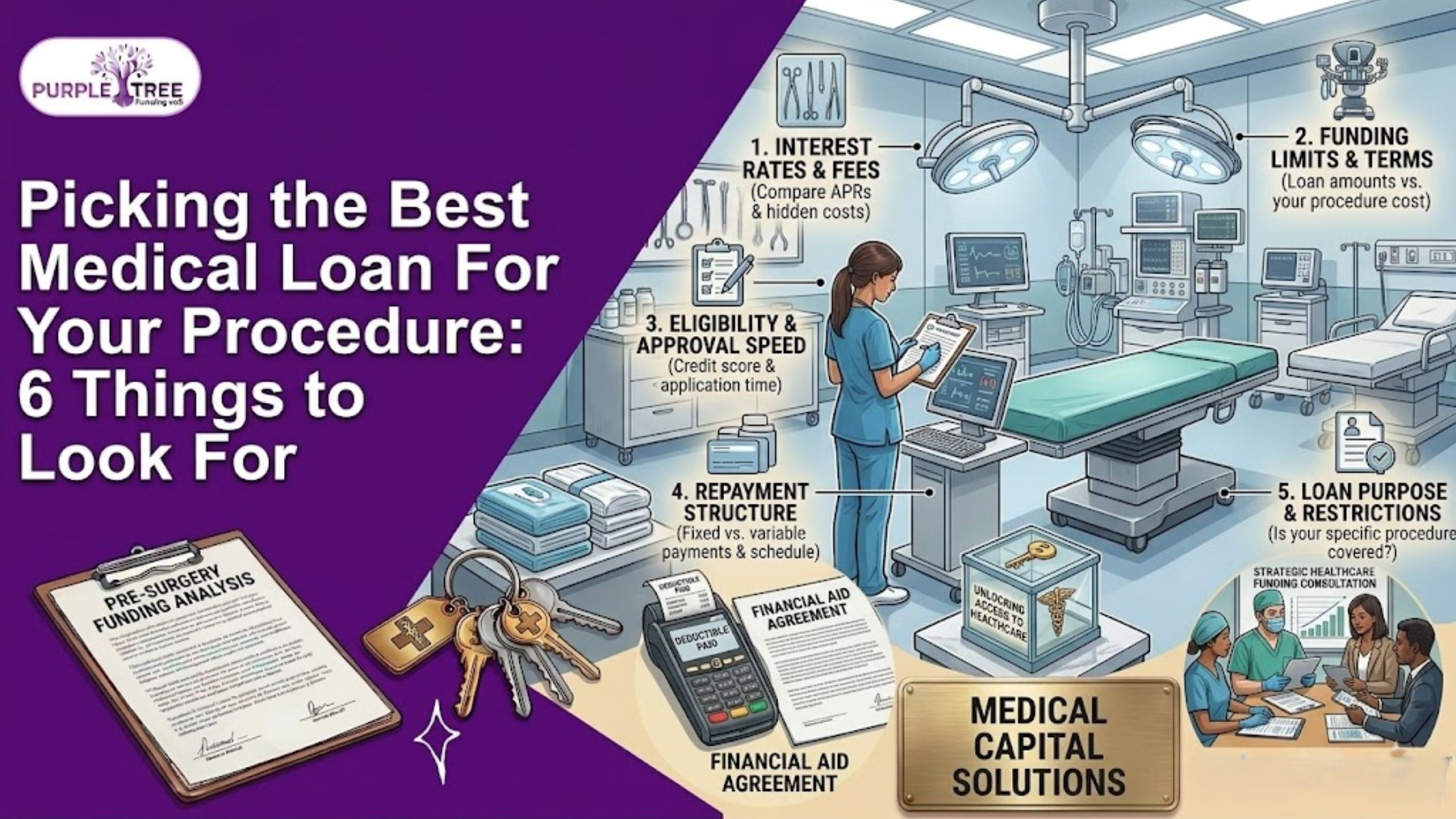

5. Transparent Costs and No Hidden Fees

The headline rate is only part of the picture. Before committing, get the full cost in writing:

- Total repayment amount, not just the rate

- Origination, processing, or administrative fees

- Prepayment penalties, if any

- Whether the rate is fixed or variable

A slightly higher rate on a transparent, well-structured product often costs less than a "cheap" loan loaded with fees and penalties. Clarity up front is itself a signal of a lender worth working with.

6. A Lender That Understands Healthcare

General business lenders treat a medical practice like any other borrower. A lender experienced in healthcare understands reimbursement cycles, equipment costs, regulatory realities, and the specific pressures of running a clinic, dental office, or veterinary practice.

That understanding shows up in better-fit terms, faster approvals, and fewer surprises. When you're comparing options, weigh industry experience heavily; it's the difference between a funder who works around your practice and one who simply processes your application.

Common Mistakes Practices Make When Borrowing

Even strong practices stumble on financing. The most frequent errors:

- Borrowing without a clear return: Tie every dollar to a measurable outcome, equipment that adds billable capacity, staff that reduces wait times, and a buildout that grows patient volume.

- Choosing a rate alone: A low rate on the wrong structure costs more than a fair rate on the right one. A fixed-term loan covering a recurring reimbursement gap is a classic mismatch.

- Waiting until it's urgent: Applying mid-crisis limits your options and weakens your position. The strongest time to secure funding is before you're forced to.

- Over-borrowing: Take what the plan needs, not the maximum offered. Idle capital still costs you in repayments.

When to Finance vs. Pay Out of Pocket

Not every purchase belongs on a loan, and not every reserve should be drained. The decision comes down to opportunity cost.

Financing makes sense when the purchase generates revenue faster than the cost of the capital for new equipment that opens a billable service line, or an expansion that grows patient volume. It also makes sense when paying cash would leave your practice short on the working capital it needs to absorb a slow reimbursement cycle.

Paying out of pocket fits small, non-revenue purchases or when you're sitting on reserves well beyond your operating buffer. The test: would financing this free up cash to put toward something that earns more than the loan costs? If yes, finance it and protect your liquidity.

Preparing Your Practice to Apply

A little preparation speeds approval and strengthens your terms. Before you apply, have ready:

- Recent bank statements: Typically, the last few months, the core of revenue-based underwriting

- Basic practice details: Time in business, entity structure, monthly revenue

- A clear use of funds: lenders respond better to a specific plan than a vague "growth" request

- Your current obligations: Knowing your existing debt service helps you borrow the right amount

Final Thoughts

The best medical and healthcare loan isn't the one with the lowest advertised rate; it's the one that funds fast enough to matter, fits how healthcare cash flow actually moves, and comes from a lender who understands your business. Run any option through these six checks: speed, the right product, healthcare-aligned terms, sensible approval criteria, transparent costs, and genuine industry experience. Six clear yeses, and you can move forward with confidence.

If you're financing equipment, covering a working-capital gap, or investing in growth, Purple Tree Funding offers medical practice financing built around how healthcare businesses operate, with fast decisions and terms that fit your cash flow.

FAQ’s

What can I use a medical and healthcare loan for?

Almost any practice needs purchasing equipment, covering payroll during slow reimbursement cycles, renovating or expanding, hiring staff, or managing day-to-day operations. Medical equipment financing is tied to a specific purchase, while healthcare working capital is unrestricted and covers whatever keeps the practice running.

How fast can I get medical practice financing?

Faster than a traditional bank. Lenders that underwrite on your practice's revenue and cash flow often issue a decision within 24 to 48 hours, with funds following shortly after. That speed matters when equipment fails or a time-sensitive opportunity appears.

Do I need perfect credit to qualify?

No. Industry-focused lenders weigh your practice's consistent revenue and healthy deposits more heavily than a flawless personal credit score. The stability of an established healthcare business often carries more weight than collateral or credit history alone.

What's the difference between medical equipment financing and working capital?

Medical equipment financing funds a specific asset, such as imaging, dental, or diagnostic equipment, and the equipment usually secures the loan. Healthcare working capital is flexible cash for payroll, supplies, or bridging reimbursement gaps. Choose equipment financing for one defined purchase, or working capital when you need funds to operate or grow.

Can a new or growing practice qualify for financing?

Yes. While a longer time in business strengthens an application, many lenders fund younger practices as long as revenue is consistent and cash flow is healthy. Steady deposits matter more than years of operating history.