Electricians across the U.S. keep homes, businesses, and infrastructure powered, but keeping their businesses energized requires more than technical skills. Whether you’re expanding operations, investing in new equipment, or simply stabilizing cash flow, getting an electrician business loan can make a significant difference. But what exactly do lenders look for in an electrician business loan application?Getting approved for a business loan isn’t just about asking for money; it’s about showing lenders you’re wired for success. From your credit score to your annual revenue, they examine the whole circuit of your financial profile before flipping the switch on approval (U.S. Small Business Administration, 2025). So, if questions like “how do I qualify for an electrician loan?” or “what paperwork do I need?” are sparking in your mind, you're in the right place. This guide breaks down exactly what lenders look for, plus how to sharpen your application and get the funding your electrical business deserves.

Why Do You Need to Apply for an Electrician Business Loan?

If you want to expand your business, regardless of the type of business you have, electrical business funding can make it happen for you. The Electrician contractors operate in a highly skilled and capital-intensive industry. While jobs may be profitable, the upfront costs and delayed payments can squeeze cash flow. Common reasons electricians apply for small business loans include:

- Purchasing new tools, vehicles, or electrical equipment

- Hiring and paying additional crew during high-demand seasons

- Covering insurance, licensing, or certification renewals

- Marketing and local advertising expenses

- Handling delayed payments from commercial clients

- Managing emergency repairs or replacements

Without working capital, even successful electrical businesses can hit a wall. That’s why securing the right financing at the right time is critical. Electricians exploring different loan options can choose from equipment financing, lines of credit, or unsecured loans tailored to their business needs.

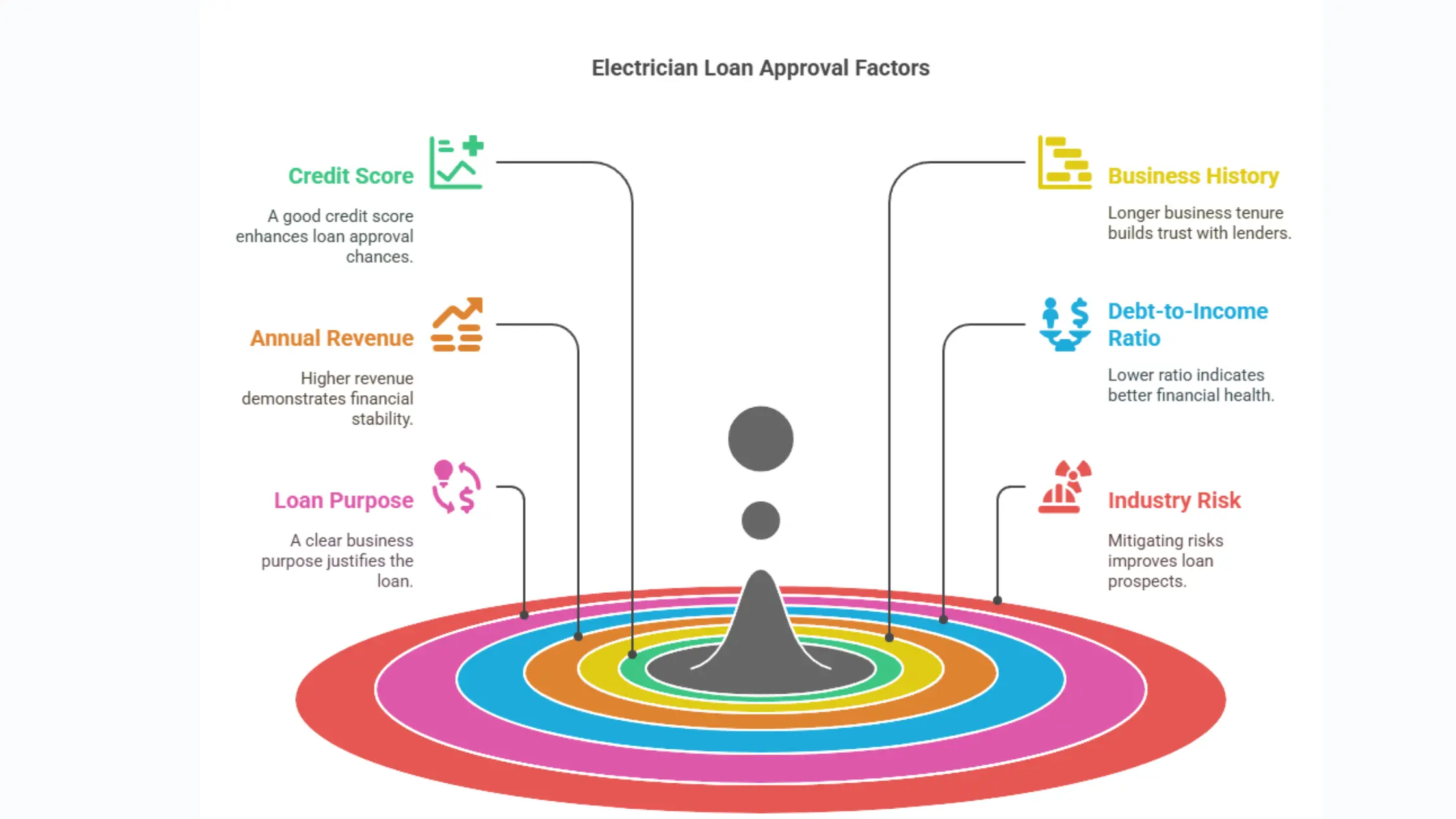

What Lenders Evaluate in Electrician Business Loan Applications?

The traditional electrical business financing approval is usually based on both the credit score history and business history. If you are not already an established electrician with steady cash flow, it will be difficult for you to get approved for one of these loans. Lenders, whether traditional banks or alternative financing companies, use several criteria to evaluate the strength of your application.Here’s what they’re looking for:

1. Credit Score (Personal and Business)

The business loans for electricians typically include the lender’s review of both your personal credit score and business credit profile. A score of 650+ may improve access to traditional loans, while alternative lenders may approve lower scores for short-term loans or merchant cash advances.

2. Time in Business

Most lenders require at least 6 months to 2 years of operating history. Longer business tenure helps establish trust and reduces perceived risk.

3. Annual Revenue

Your gross monthly or annual revenue shows how much cash flows through your business. The next question that appears after that is How Much Can You Borrow for an Electrician Business?. Many lenders establish minimum revenue thresholds (e.g., $10,000 per month or $120,000 per year) for approval of electrician loans.

4. Debt-to-Income Ratio

If you already have existing debts (equipment leases, credit lines), lenders will assess your ability to take on more. A lower debt-to-income ratio signals healthier finances.

5. Loan Purpose

Lenders want to see that your loan request has a valid business purpose—equipment upgrades, expansion, cash flow stabilization, or marketing growth plans.

6. Industry Risk

Trades like electrical work can be considered moderate risk due to physical hazards and economic fluctuations. A solid client base, licenses, and good reputation help mitigate that risk.Pro Tip: Understanding the full loan process can help electricians avoid delays and improve their chances of fast approval. Before applying, it's important to know your potential funding limits based on revenue, credit score, and time in business.

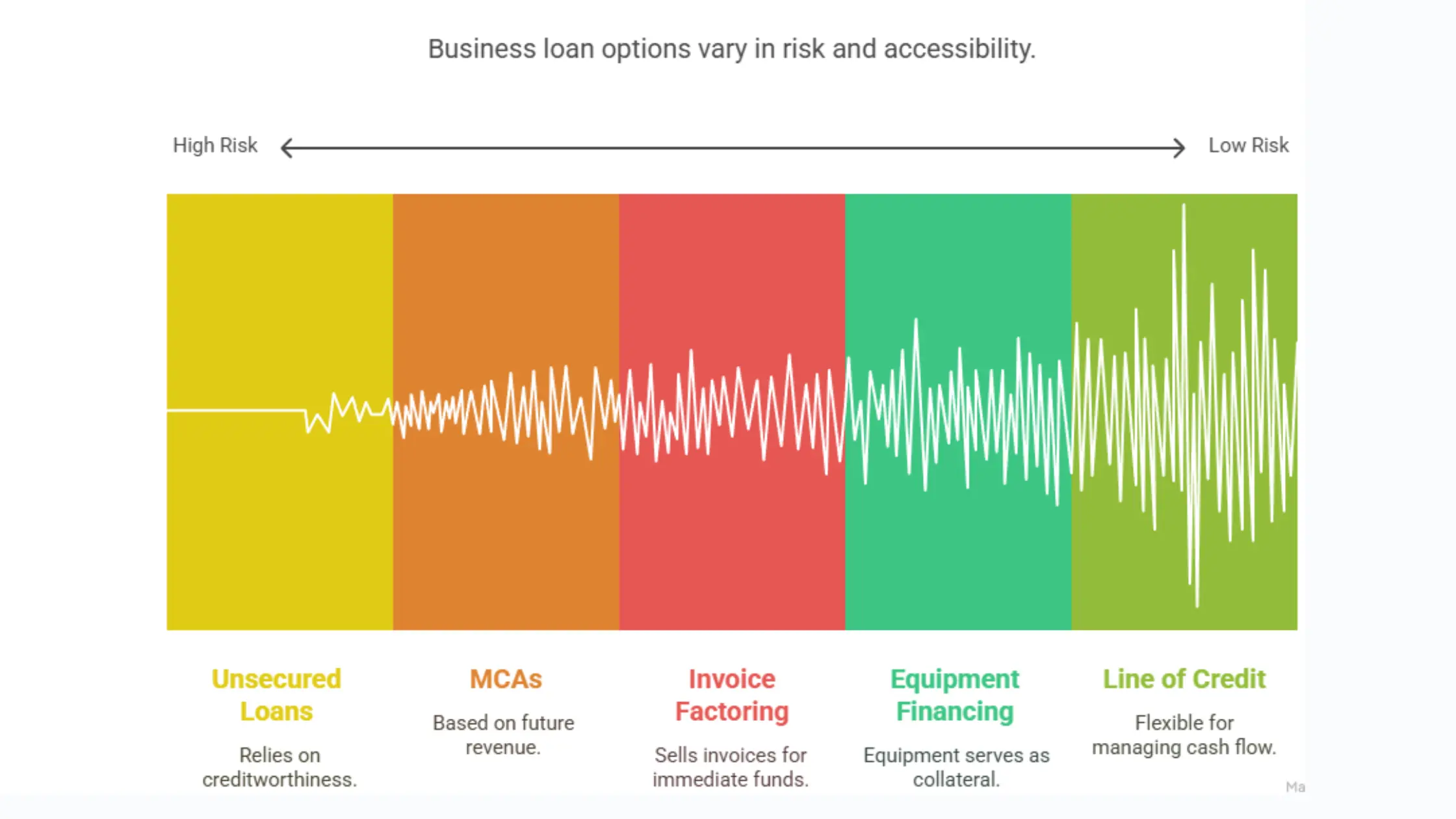

What are the Common Business Loan Options for Electricians?

Depending on your needs and qualifications, different types of electrical contractor business loans may be available. Here are the most common:

- Unsecured Business Loans

Ideal for electricians without collateral. These loans rely on creditworthiness and cash flow rather than physical assets.

- Merchant Cash Advances (MCAs)

A quick funding option based on your future revenue. While MCAs are easy to qualify for, they carry higher repayment costs.

- Equipment Financing

Use this to purchase vans, ladders, generators, or power tools. The equipment itself serves as collateral.

- Business Line of Credit

A flexible option for managing cash flow or covering unexpected expenses. You only pay interest on the amount used.

- Invoice Factoring

If you're waiting on client payments, this lets you sell your invoices to a lender in exchange for immediate funds.Each funding type has pros and cons, and working with a specialist lender like Purple Tree Funding can help you match with the right solution for your unique needs.

How to Strengthen Your Electrician Loan Application?

If you want to improve your chances of approval, take the following steps before applying:

- Organize financial documents: Have recent tax returns, bank statements, and profit and loss reports ready.

- Maintain a clear business plan: Explain how the funds will be used and the expected ROI.

- Pay down existing debts: The lower your debt load, the better, where possible, before applying.

- Separate business and personal finances: Use a dedicated business bank account.

- Check your credit score: Address any errors and improve your score before applying.

These small steps can go a long way in proving to lenders that you’re a responsible borrower.

Mistakes Electricians Should Avoid When Applying for a Loan

Many small business owners unknowingly make errors that derail their loan application. Here's what to avoid:

- Not knowing your numbers: Be ready to discuss your average monthly revenue and expenses.

- Applying for the wrong loan type: Equipment financing won’t work for marketing expenses.

- Overborrowing: Requesting too much can raise red flags.

- Incomplete paperwork: Missing documents delay or disqualify your application.

- Ignoring alternative lenders: Traditional banks aren't your only option; consider private lenders who specialize in understanding trade businesses.

Even if you have some queries to get the answers to your queries, like what exactly you need for the business loan applications, here is the set of questions:

1. Can electricians qualify for small business loans with bad credit?

Yes. While bad credit may limit traditional loan options, alternative lenders like Purple Tree Funding can still offer MCAs or unsecured loans based on revenue and business health.

2. What paperwork is needed for an electrician loan?

Typical documents include bank statements, business license, tax returns, financial statements, and a voided check. Each lender may vary.

3. How fast can I get funding?

With online lenders like Purple Tree Funding, you can get approved and funded in as little as 24 to 48 hours, depending on the loan type.

4. What is the minimum revenue required?

Most lenders prefer electricians earning at least $10,000 per month; however, exceptions may exist depending on other factors, such as time in business and credit profile.

5. Do I need collateral to get a business loan?

Not always. Unsecured business loans do not require collateral, though you may pay slightly higher interest rates for the added risk.

Why Electricians Trust Purple Tree Funding?

At Purple Tree Funding, we specialize in helping electricians and trade businesses secure fast, flexible, and transparent electrician financing. Whether you're a solo operator or run a growing electrical crew, we make funding simple—with:

- Lightning-fast approvals (often within 24 hours)

- Flexible repayment options

- No collateral requirements on unsecured loans

- Dedicated advisors who understand the electrical industry

- Access to a wide range of loan products in one place

We’re not just lenders, we’re partners in your success.

Final Thoughts

Electricians are the backbone of modern infrastructure, but to keep growing, funding is often essential. Lenders look at your credit score, business history, cash flow, and loan purpose, so preparation is key.Whether you're looking to buy new equipment, hire staff, or manage cash flow, Purple Tree Funding is here to help with fast, tailored financing options designed specifically for tradespeople.

FAQs

Q1. What credit score is needed for an electrician business loan?

Most traditional lenders prefer a credit score of 680 or higher, but alternative lenders may approve electricians with scores as low as 600, especially for short-term or unsecured loans.

Q2. How much revenue do I need to qualify for a loan?

Lenders typically look for a minimum of $10,000 in monthly revenue or $120,000 annually, though some options are available for businesses with lower earnings through flexible lenders.

Q3. What documents do I need to apply for an electrician loan?

Common documents include bank statements (3–6 months), tax returns, business license, financial statements, and a voided check. Having a business plan can also strengthen your application.

Q4. Can I get a loan for my electrician business with no collateral?

Yes, many unsecured electrician business loans don’t require collateral. However, they may have slightly higher interest rates due to the increased risk to the lender.

Q5. How fast can I get approved and funded?

With lenders like Purple Tree Funding, approval can take as little as 24 hours, and funding may follow within 24 to 48 hours, depending on the loan type and documentation readiness.